SMM November 23:

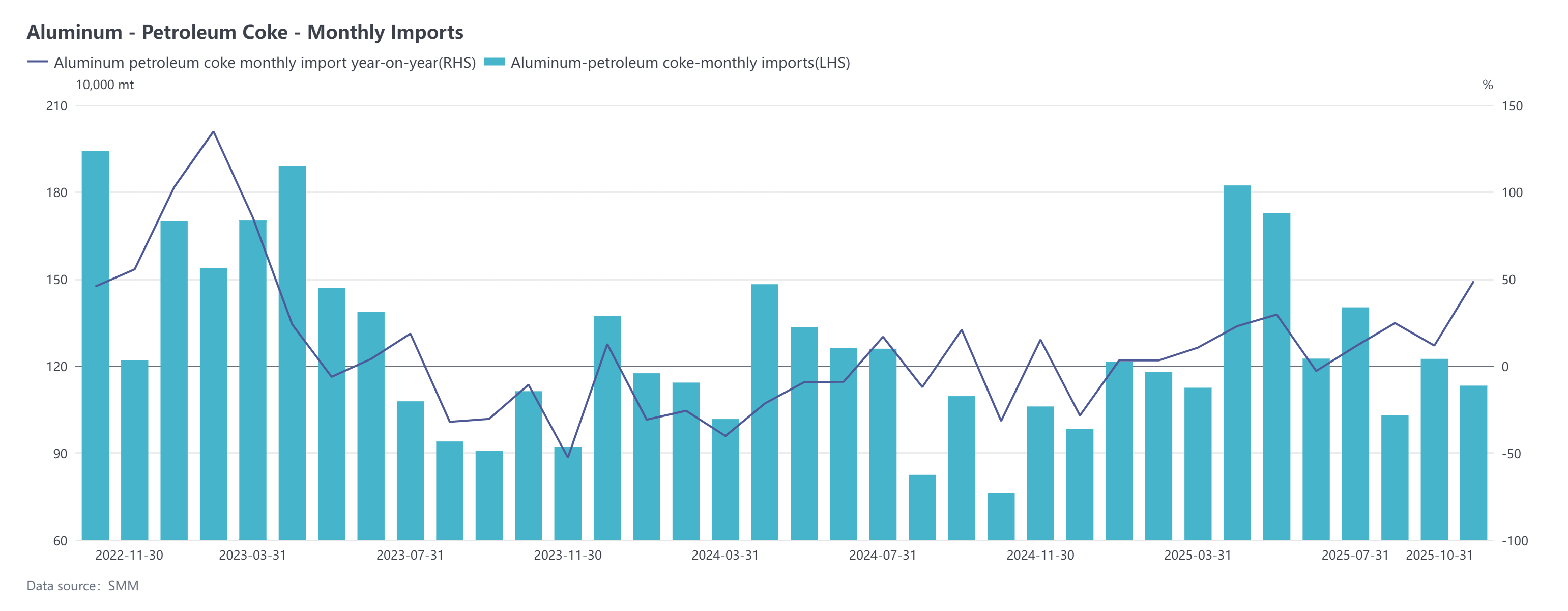

Customs data showed that China's petroleum coke imports in October 2025 reached 1.1324 million mt, down 7.54% MoM but up 48.76% YoY. The estimated average import price for petroleum coke in October was $225.02/mt, up 5.47% MoM and 60.97% YoY. Cumulative petroleum coke imports for January-October 2025 totaled approximately 13.0862 million mt, up 15.24% YoY.

By import source, China's main petroleum coke suppliers in October 2025 were Russia (240,000 mt, 21%), the US (175,000 mt, 15%), and Saudi Arabia (105,800 mt, 9%).

Import prices showed a mixed performance in October, with the average price at about $225.02/mt, up 5.47% MoM. Among the 20 source countries/regions, 14 had continuous import volumes. Prices for imports from the US, Canada, and Romania rose significantly, with increases exceeding $30/mt, while prices for imports from Indonesia, Kazakhstan, and Brazil declined noticeably. Indonesian petroleum coke saw the largest price drop, falling by over $90/mt.

Since Q4, the domestic petroleum coke market supply side has shown a two-way divergence characterized by accelerated domestic capacity release and shrinking import supply replenishment, with the market supply-demand pattern undergoing phased adjustments. Domestically, Q4 saw a marked slowdown in refinery maintenance pace and a significant reduction in new maintenance plans, while the production resumption process at previously idled refineries accelerated, and some long-term idled enterprises gradually resumed production, leading to a continuous rebound in domestic petroleum coke output scale and a gradual emergence of incremental supply effects. Demand side, since November, as petroleum coke prices climbed to high levels, downstream enterprises' purchase willingness cooled, and market procurement pace turned cautious, creating some digestion pressure for the domestic supply increment. The fundamentals of the domestic petroleum coke market failed to provide a solid foundation for petroleum coke imports, coupled with international trade adjustments. US imported coke volume is expected to continue declining due to rising costs, and international petroleum coke prices remain high, further dampening import procurement enthusiasm. Overall, domestic petroleum coke imports in November are highly likely to maintain a downward trend.

![Aluminum Scrap Prices Follow Upward Trend but with Regional Divergence Market Supply Increases [SMM Cast Aluminum Alloy Morning Comment]](https://imgqn.smm.cn/usercenter/wStpx20251217171650.jpg)